How Tenant Protection and Insurance Plans Help Pre-Define Liability and Reduce Operational Headaches for Self-Storage Operators

Every self-storage owner has dealt with upset tenants after their stored property was damaged. Maybe it was the businessman whose inventory was ruined after a pipe burst. Or the family distressed about their belongings being destroyed by rodents. These situations are challenging enough at the counter – but they can escalate into time-consuming legal disputes that drain resources and damage your reputation.

At the 2025 ISS World Expo, industry attorneys highlighted that disputes over damaged tenant property remain one of the top operational challenges for self-storage facility owners.⁶ Many of these disputes stem from tenants seeking to gain compensation from facility operators after the losses occur, often with no clear process or coverage limits in place.

Defining Your Limits and Claim Process

Tenant protection and insurance programs help you manage risk differently but achieve the same goal: establishing clear coverage limits and claims processes before losses occur. Protection plans allow you to offer an enhanced lease with limited liability, while insurance programs enable tenants to purchase their own policies through your facility.

Understanding What Your Facility Insurance Does (and Doesn't) Cover for Tenant Property

Many storage owners misunderstand what their commercial property & casualty (P&C) insurance covers when it comes to tenant belongings. Here's what you need to know:

Your property insurance covers damage to your buildings and structures. If a pipe bursts or fire damages your facility, your property insurance responds.

Your Commercial General Liability (CGL) insurance covers bodily injury claims and property damage to others – but specifically excludes property in your care, custody, or control.¹ This means tenant belongings stored at your facility are not covered by your CGL policy.

This exclusion exists because insurance companies view stored belongings as being under your control, similar to how a mechanic has custody of cars in for repair. Even if you did nothing wrong, your CGL won't cover tenant property losses.¹

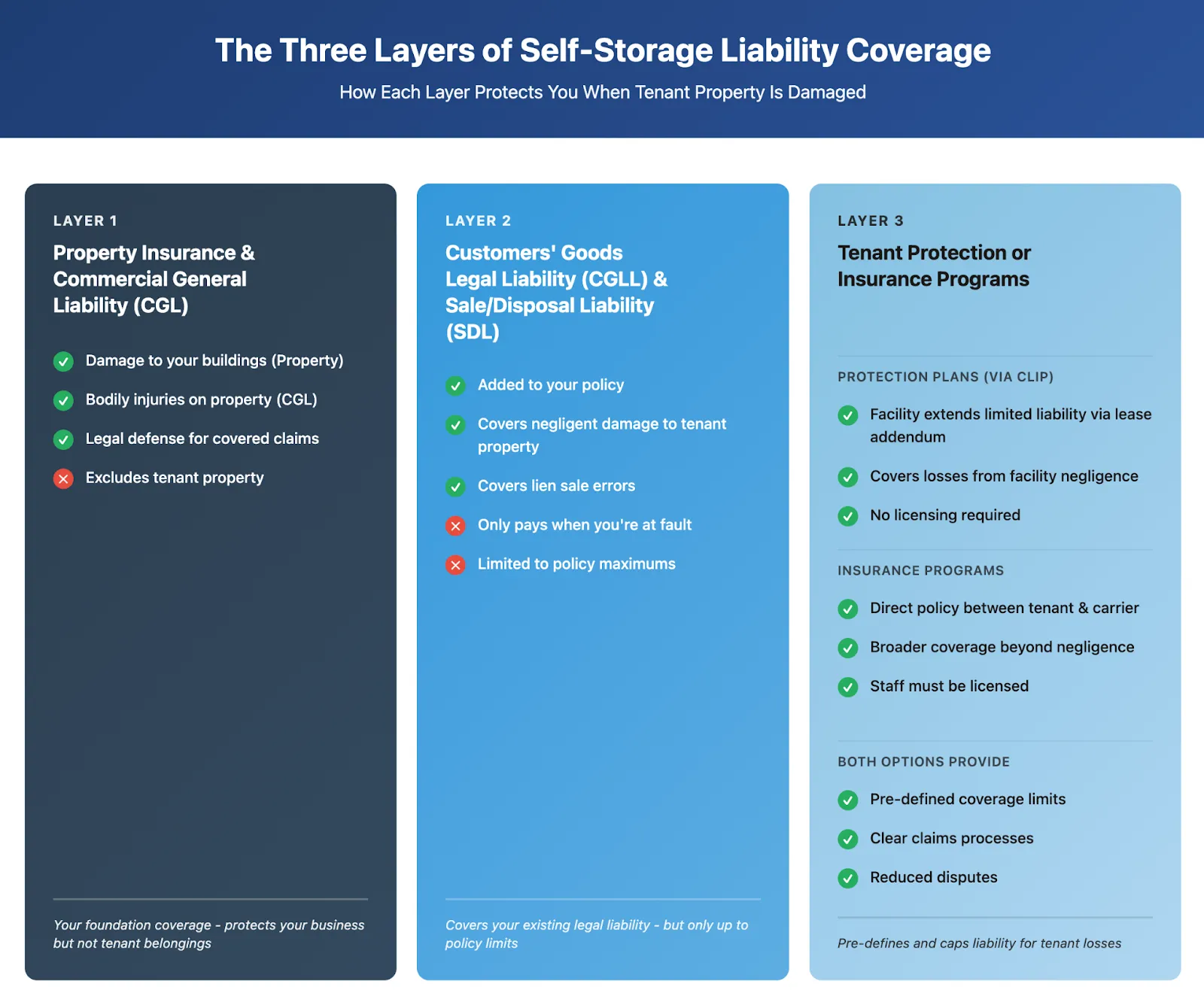

The Three Components of Comprehensive Coverage

A complete risk management approach for self-storage involves three distinct components:

1) Your Self-Storage Facility Insurance (Property & CGL): Your property insurance and Commercial General Liability (CGL) policy form the foundation, covering your buildings and liability for bodily injuries – but not tenant belongings (due to the care, custody, or control exclusion).

2) Customers' Goods Legal Liability (CGLL) and Sale & Disposal Liability (SDL): These are specialty coverages that every self-storage owner should add to their general liability policy.

CGLL responds when you're found legally liable for damaging tenant property through negligence – for example, if you knew about a roof leak and failed to repair it.

SDL covers procedural errors during lien sales. These coverages typically range from $25,000 to $1 million and only pay when you're at fault.² ³ ⁴

3) Tenant Protection or Tenant Insurance Plans: These programs ensure tenants have defined coverage for property losses.

Protection plans are lease addendums where the facility extends limited liability for losses caused by facility negligence (maintenance failures, security lapses). The facility is backed by a Contractual Liability Insurance Policy (CLIP) that transfers this risk to an insurance carrier. No insurance licensing required.

Insurance programs involve partnering with a licensed carrier to offer actual insurance policies to tenants. This provides broader coverage but requires facility staff to be licensed. State insurance departments regulate pricing and coverage terms.

With either option, tenants pay additional fees - as rent (protection) or premiums (insurance).⁵

Note: Tenant Protection Plans are essentially premium lease agreements - for additional rent, you agree to assume limited liability if your facility's negligence causes damage. Tenant Insurance Plans are a separate contract between the tenant and an insurance company that covers various perils regardless of fault.

How Tenant Protection & Insurance Plans Work

Tenant Protection Plans:

Tenant protection plans are not insurance policies purchased by tenants. They are three-party agreements between the tenant, facility operator, and the insurance carrier backing the plan through a CLIP.

Here's the structure: Your facility offers an optional lease addendum that extends your liability for certain types of losses. The facility is backed by a CLIP that transfers this risk to an insurance carrier. Tenants who opt in pay additional rent (not an insurance premium) for this extended protection.

When a loss occurs that may involve facility responsibility – say water damage from a burst pipe due to deferred maintenance – the process is:

- The tenant reports the damage

- They file a claim with the protection plan administrator

- The claims process determines if the facility bears responsibility

- If covered, the tenant receives compensation within the plan's pre-defined limits

The protection plan clearly defines what situations are covered (typically those involving facility negligence like maintenance failures, security lapses, or damage during facility-controlled work) and sets maximum liability amounts from the start.⁵

Tenant Insurance Plans:

Tenant insurance involves the facility obtaining a master insurance policy, with tenants added as additional insureds. Key differences from protection plans:

- Tenants receive a certificate of insurance (not individual policies)

- Coverage includes various perils beyond facility negligence (fire, theft, weather events)

- Requires facility staff to be licensed to sell insurance

- Regulated by state insurance departments with fixed pricing

- The insurance carrier, not the facility, assumes the risk

Think of the difference this way: Protection plans offer tenants an upgraded lease where the facility agrees to assume limited liability for specific situations. Insurance offers tenants their own policy that covers a broader range of risks. Both achieve the same goal for facilities: pre-defined coverage limits and clear claims processes that reduce disputes.

Real-World Scenarios

Consider these common situations:

Scenario 1 - Burst Pipe: A pipe bursts due to deferred maintenance, damaging contents in several units. Without a tenant protection or insurance plan, affected tenants may pursue unlimited claims. Your CGL excludes their property. Your CGLL would respond but only up to policy limits. With a protection or insurance plan in place, your liability to all of the impacted tenants is capped by the plan terms.

Scenario 2 - Construction Mishap: During roof replacement, contractors fail to properly protect units and roofing materials damage stored items. Via the claims process, the protection plan would determine whether the facility failed to supervise contractors properly, and then provide coverage within defined limits.

Scenario 3 - Gate Malfunction: An issue with your gate that you knew about, but hadn't repaired yet, allows a thief to break-in. Protection and insurance plans provide a clear process for determining facility responsibility and compensating tenants within pre-agreed limits.

The Operational Benefits

When tenants have coverage, it creates operational efficiency:

- Pre-defined liability limits: Instead of facing unlimited claims, you know your maximum exposure

- Standardized claims process: Rather than case-by-case negotiations, there's a consistent procedure

- Reduced manager stress: Staff can focus on helping tenants through the established claims process rather than defending against open-ended demands

- Preserved customer relationships: When the facility is found responsible, tenants receive compensation within pre-agreed terms with low deductibles (typically $100)

- Clear documentation: Protection plans maintain claims records that can be useful if disputes escalate

These plans don't eliminate all disputes – tenants may still have concerns even after receiving compensation. However, having an established claims process with pre-defined limits significantly reduces conflict and uncertainty.

Implementation Considerations

Successful protection plan programs require thoughtful implementation:

Coverage Verification: If tenants claim existing coverage through homeowners or renters policies, establish a simple verification process. Many tenant protection plan operators use compliance systems that can verify private policy details and alert you when coverage lapses.⁷

Consistent Application: Whether you require protection plans or make them optional, consistency is key. Train staff on how to explain the benefits clearly and transparently.

Phased Rollout: Many operators start by offering protection or insurance plans to new tenants only in order to avoid disrupting existing relationships, and then expand based on results.

Licensing Requirements: Protection plans require no special licensing, making them simpler to implement. Insurance programs offer broader coverage, but require facility staff to obtain and maintain insurance licenses, with ongoing regulatory compliance.

Addressing Common Concerns

"Will this impact occupancy?" Many operators report that when positioned as protection for stored belongings with clearly defined coverage, customers understand the value. Focus on transparency about what the plan covers and your liability limits.⁷

"Our state caps liability." Statutory liability caps provide some protection, but disputes about whether those caps apply to your specific situation or whether you followed proper procedures can still arise. Protection and insurance plans provide clarity where statutory caps may be contested or vary by jurisdiction.

"We have Consumer Goods Legal Liability coverage - isn’t that enough?" CGLL only covers your existing legal liability up to policy limits. Protection and insurance plans allow you to extend limited, defined liability for specific situations (like maintenance failures or security lapses) while clearly capping your exposure. Bottom line: both tenant protection plans and tenant insurance plans give your tenants a path to compensation while protecting you from unlimited liability claims.¹

Making the Business Decision

Implementing tenant protection or insurance plans is fundamentally about risk management. Consider the time spent handling disputes over damaged tenant property, the stress on your team, and the potential impact on your reputation. Comprehensive tenant protection and insurance strategies with clearly defined liability limits are becoming standard practice.⁶

The question for operators is not whether tenant property losses will occur – they will. The question is whether you have systems in place to pre-define your liability and handle claims efficiently while maintaining positive customer relationships.

Sources

- Legal Liability Coverage Form – An Often-Overlooked Form, IRMI, 2025. https://www.irmi.com/articles/expert-commentary/legal-liability-coverage-form-an-often-overlooked-form

- 10 Insurance Coverages Your Self-Storage Business Needs Today, Inside Self-Storage, 2024. https://www.insideselfstorage.com/insurance/10-insurance-coverages-your-self-storage-business-needs-today-plus-when-and-how-to-update-your-policy

- Sale & Disposal Liability – market limits examples, StorageFirst application, 2024. https://www.storagefirst.com/media/hmkdgs3u/selfstorageapp-2024.pdf

- CGLL limits in practice, market overviews (MiniCo and program sites), 2023–2025. https://www.minico.com/4-specialized-insurance-coverages-for-self-storage-businesses

- Why Self-Storage Operators Should Consider a Tenant-Protection Plan, Inside Self-Storage, 2024. https://www.insideselfstorage.com/insurance/why-self-storage-operators-should-consider-a-tenant-protection-plan-plus-how-they-work

- Reduce Your Risk of Being Sued! ISS seminar video + presentation, 2025. https://www.insideselfstorage.com/iss-brand/reduce-your-risk-of-being-sued-let-this-seminar-help-you-keep-your-self-storage-business-out-of-court Presentation: https://www.issworldexpo.com/content/dam/markets/na/iss-world-expo/2025/powerpoints/risk-management-track/Klasing%20Self-Storage%20Lawsuits.pdf

- Proven Strategies to Boost Tenant Coverage Enrollment Rates, SafeLease, 2025. https://www.safelease.com/resources/proven-strategies-to-boost-tenant-coverage-enrollment-rates